Thursday, 1 April 2021

Wednesday, 31 March 2021

Stimulus, tax scams are everywhere: What to watch for

Consuming lunch the opposite day with my co-workers at our bungalow-turned-home-office, I obtained interrupted by a telephone name from somebody claiming to be from my TV service firm.

Uninterested in the scammers, I requested the man on the road in regards to the climate there after which advised him how we might repair his air conditioner if he put $500 on a present card for Residence Depot after which advised him how he’d have to learn me these numbers.

“Come on,” I egged him on, “you know the way to do that. You have been telling folks how to do that for years.”

Yeah, the pandemic can drive you a bit excessive. My son, the accountant, and my husband, the editor, simply shook their heads. My son later advised me: “Nice mother, now the man’s going to get again at us by submitting a faux tax return.”

And so it has come to this: We’re both getting scammed by these guys or getting labored up when these guys hold calling. And sure, we marvel what they could do subsequent.

Now that it’s tax season, scammers will use one scheme after one other to craft stimulus scams, file phony tax returns to steal tax refund money or stage some drama to scare us into handing over our Social Safety numbers, checking account numbers and money.

The most effective recommendation stays to easily dangle up the telephone on scammers, and do not interact with their texts.

The three rounds of stimulus funds supply customers monetary aid in the course of the pandemic, however additionally they give scammers one other storyline.

Amy Nofziger, director of sufferer help for the AARP Fraud Watch Community, stated one shopper was contacted by somebody supposedly from USATaxHelp12@gmail.com who reportedly had a strategy to expedite a stimulus fee.

The buyer sadly signed an digital doc, and now the scammers have his e-signature. Be cautious in the event you obtain an electronic mail stating that you’ve paperwork to signal. Should you haven’t requested any paperwork, it’s seemingly a phishing assault.

One other clue: A legit enterprise hardly ever makes use of a web-based Gmail or Yahoo account.

The IRS is not sending texts about stimulus cash

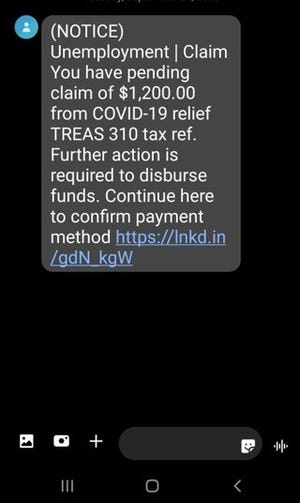

Sarah Kull, particular agent answerable for the Inside Income Service Felony Investigation Division of the Detroit area workplace, warns of an uptick in Financial Affect Fee schemes, together with textual content messages that ask taxpayers to reveal checking account data.

One textual content despatched by scammers famous: “You may have a pending declare of $1,200.00 from COVID-19 aid TREAS 310 tax ref.”

Once more, texts aren’t a part of actual stimulus rollout packages. But somebody who’s uncertain about how or once they would possibly obtain a stimulus fee would possibly wrongly imagine the textual content is legit.

The phony textual content signifies: “Additional motion is required to just accept this fee. … Proceed right here to just accept this fee …”

Should you pressed the hyperlink, you ended up at a phishing net deal with. One faux hyperlink, in response to an IRS warning in November, took folks to a faux web site that appears just like the Get My Fee web site at IRS.gov.

If folks go to the faux web site and entered their private and monetary account data, the IRS warned, the scammers might acquire that information to make use of in ID theft-related crimes.

Extra:Social Safety scammers now textual content photos of phony badges

Extra:Not as many Individuals eligible for third stimulus verify: Here is what it is advisable to know

The IRS stated individuals who obtain this textual content rip-off ought to ship a screenshot in an electronic mail to phishing@irs.gov. You’d embody if you obtained the textual content message, the telephone quantity it supposedly got here from, and the telephone quantity that obtained the textual content.

Rip-off warning: The IRS is not going to ship a textual content regarding a stimulus fee or a textual content asking you to share your checking account data.

Do not pitch an odd 1099

Many retirees and others had been shocked once they obtained a 1099-G within the mail to report unemployment advantages on their tax returns this yr.

One caller to the AARP Fraud Watch Community Helpline famous that the 1099-G that he obtained indicated he wanted to report $2,400 in jobless advantages, Nofziger stated. However the man had been retired for 17 years and did not file for unemployment advantages in 2020. As an alternative, somebody used his private data to file a declare.

“Lots of these victims had been unaware they had been victims till the 1099-G got here out,” she stated.

“It is very jarring for folks to obtain this type.”

You do not wish to ignore a 1099-G. Contact the state unemployment workplace to report the fraud and get a corrected 1099-G that exhibits you didn’t get any advantages.

The IRS states that victims of ID theft mustn’t report earnings that they did not obtain even when they haven’t but been capable of get a corrected 1099-G earlier than submitting their tax returns.

Extra:Properly-known Michigan lawyer’s ID stolen in Ohio unemployment rip-off

Extra:Faux jobless claims now set off tax troubles for victims

Do not decide a scammer to do your taxes

Sadly, unhealthy actors pop up throughout tax season, possibly somebody you have met by a pal of a pal, pretending to give you an awesome deal or promising to get you an additional massive tax refund.

Nofziger famous {that a} man reported in early March a few tax preparer discovered by Fb.

After having a tax return accomplished, the tax preparer stated the refund was $1,000 lower than the tax refund listed on their 1040. One way or the other, the charges are a lot greater than initially quoted. The tax preparer needs a refund deposited into one in every of her accounts after which plans to chop a verify and ship the taxpayers their refund.

No shock, the taxpayers are actually having bother reaching this particular person and getting a standing on their return.

“They seemed up the routing variety of the account that it’s alleged to be deposited into and stated it seems to be like some form of wire switch routing quantity,” Nofziger stated.

The IRS says that regardless that most tax return preparers present trustworthy service, some trigger nice hurt by fraud, identification theft and different scams yearly.

Dishonest preparers can steal your private ID data, possibly Social Safety numbers in your youngsters; and a few would possibly even steal a significant a part of your tax refund.

One pink flag: A tax preparer who does not have to see a W-2 or different paperwork. You don’t need a tax preparer to invent earnings so you’ll be able to qualify for tax credit.

By no means signal a clean tax return or one which’s not accomplished. Evaluation the routing and checking account quantity on the finished return. Try to be getting the tax refund, not the tax preparer.

The IRS warns: “Ghost preparers do not signal the tax returns they put together. They might print the tax return and inform the taxpayer to signal and mail it to the IRS.”

Paid preparers are required to signal and embody their preparer tax identification quantity on the return. “Not signing a return is a pink flag that the paid preparer could also be trying to make a quick buck by promising a giant refund or charging charges based mostly on the scale of the refund,” the IRS warns.

Additionally the IRS warns: “Don’t assume web commercials, pop-up adverts or e-mails are from respected corporations.”

Volunteers from tax preparation packages will help many individuals. The AARP Basis Tax-Aide program, for instance, presents in-person and digital tax help to anybody freed from cost with a particular concentrate on taxpayers who’re over 50 or have low to reasonable earnings. This yr, tax help is offered by appointment solely. See aarpfoundation.org/taxaide.

Or see IRS.gov and the record of Volunteer Earnings Tax Help websites for individuals who qualify based mostly on earnings; some packages are making ready returns off-site this yr as a result of COVID-19.

Free tax assist is offered for individuals who usually make $57,000 or much less, these with disabilities and taxpayers with restricted English.

Impersonation scams proceed

Do not react to a letter or a telephone name out of the blue that appears official as a result of these reaching out to you understand you owe again taxes. Some data may be pulled by scammers from public databases or elsewhere.

Keep in mind, ID theft revolves round making issues sound credible, so the crooks typically take time to do some analysis upfront to sound like the true deal.

One essential level to recollect: The IRS will not be going to name you about again taxes that you could be owe with out sending you a written discover first. Should you’re getting a name out of the blue, it is an imposter.

“The IRS doesn’t provoke contact with taxpayers by electronic mail, textual content messages or social media channels to request private or monetary data,” in response to a brand new IRS alert.

“Usually, the IRS first mails a paper invoice to an individual who owes taxes,” the IRS acknowledged. “In some particular conditions, the IRS will name or come to a house or enterprise.”

The Michigan Division of Treasury warned in January that customers in northern Michigan had been receiving threatening tax assortment letters from scammers. The letters included this scare tactic: “Name Instantly to Forestall Property Loss.”

If the state tax debt wasn’t settled, the letter written by a scammer warned, the taxpayer’s property and Social Safety advantages might be seized.

“The piece of correspondence seems credible to the taxpayer as a result of it makes use of particular private info about their actual excellent tax debt that’s pulled straight from publicly accessible data,” in response to the state treasury.

“The scammer’s letter makes an attempt to lure the taxpayer right into a scenario the place they may make a fee to a felony.”

Do not rush to pay anybody. You do not wish to assume you are clearing up a monetary mess solely to seek out out that you just handed over your hard-earned money to a criminal.

ContactSusan Tompor via stompor@freepress.com. Observe her on Twitter@tompor. To subscribe, please go to freep.com/specialoffer. Read extra on enterprise and join our enterprise e-newsletter.

The post Stimulus, tax scams are everywhere: What to watch for appeared first on Correct Success.

source https://correctsuccess.com/finance/stimulus-tax-scams-are-everywhere-what-to-watch-for/

The child and dependent care tax credit is more lucrative than ever — but there’s one important caveat

The $1.9-trillion stimulus package deal referred to as the American Rescue Plan Act (ARPA) contains main adjustments to the longstanding federal-income-tax baby and dependent care credit score (CDCC).

Except you might be within the high-income class, the adjustments are favorable.

There’s a catch: the adjustments are short-term.

Right here’s what you should know, after first protecting some essential background data.

Baby and dependent care credit score (CDCC) fundamentals

Taxpayers with a number of qualifying people beneath their wings are eligible for the CDCC. The credit score covers eligible bills that you simply pay to look after a number of qualifying people so you’ll be able to work, or if you happen to’re married, so each you and your partner can work. When you’re married, you typically should file a joint Type 1040 for the tax 12 months in query to assert the CDCC. Nonetheless, some married however separated taxpayers are exempted from the joint-filing requirement.

Qualifying people are outlined as your under-age-13 baby, stepchild, foster baby, brother or sister, step-sibling, or a descendant of any of those people. The person should reside in your house for over half the 12 months, and should not present over half of his or her personal assist. A handicapped partner or handicapped dependent who lives with you for over half the 12 months may also be a qualifying particular person.

Typical eligible bills are funds to a day-care heart, nanny, or nursery faculty. Prices for in a single day camps don’t qualify. Prices for personal Okay-12 faculty don’t qualify, as a result of these are thought of schooling bills quite than care bills. Nonetheless, prices for before-school and after-school packages can qualify. Prices of home assist may qualify, so long as not less than a part of the prices go towards the care of a qualifying particular person.

Key level: Earlier than the ARPA, the CDCC was nonrefundable, that means it may solely be used to offset your federal revenue tax legal responsibility. When you had no legal responsibility, you bought no credit score. However for 2021, the credit score is refundable for most folk, as defined later.

See additionally: Wish to perceive the way forward for cryptos and NFTs? Register for MarketWatch’s free live event.

Expense limitation

Earlier than and after the ARPA adjustments, eligible bills can not exceed the revenue that you simply earn, or that your partner earns if you happen to’re married, from work, self-employment, or sure incapacity and retirement advantages. When you’re married, you typically should use the revenue earned by the lower-earning partner for this limitation.

So, beneath the overall limitation rule, if one partner has no earned revenue, you can not declare the CDCC. Nonetheless, in case your partner has no earned revenue and is a full-time pupil or disabled, she or he is deemed to have imaginary month-to-month earnings of $250 you probably have one qualifying particular person or imaginary month-to-month earnings of $500 you probably have two or extra qualifying people. Underneath this exception, you’ll be able to probably declare the CDCC although your partner doesn’t truly work and has no precise earnings.

Credit score limitation

Earlier than the ARPA, eligible bills (after the previous limitation) couldn’t exceed $3,000 for the care of 1 qualifying particular person or $6,000 for the care of two or extra qualifying people.

Earlier than the ARPA, the utmost credit score equaled 35% of eligible bills if the taxpayer’s adjusted gross revenue (AGI) for the 12 months was $15,000 or much less. So, for taxpayers with very modest incomes, the utmost credit score was $1,050 ($3,000 x 35%) for one qualifying particular person or $2,100 ($6,000 x 35%) for 2 or extra.

Earlier than the ARPA, the credit score fee was decreased by one share level for every $2,000 (or fraction thereof) of AGI in extra of $15,000 till the speed bottomed out at 20%. So, the credit score fee was decreased to the minimal 20% in case your AGI exceeded $43,000. The utmost credit score for folk on this revenue class was $600 ($3,000 x 35%) for one qualifying particular person or $1,200 ($6,000 x 20%) for 2 or extra.

Non permanent taxpayer-friendly adjustments

For the 2021 tax 12 months solely, the ARPA makes the next short-term adjustments.

Credit score is probably refundable

For 2021, the CDCC is refundable for taxpayers who’ve a principal place of dwelling within the U.S. for greater than one-half the 12 months. Within the case of a joint-filing married couple, both partner can meet this requirement.

Credit score might be a lot larger for many taxpayers

For 2021, the greenback limits on eligible bills for claiming the CDCC are elevated to $8,000 you probably have one qualifying particular person (up from $3,000) and $16,000 you probably have two or extra (up from $6,000).

For 2021, the utmost credit score fee is elevated to 50% (up from 35%).

However the 2021 credit score fee is decreased by one share level for every $2,000 (or fraction thereof) of AGI in extra of $125,000. So, the speed is decreased to 20% in case your AGI exceeds $183,000. Earlier than the ARPA, the AGI threshold for the credit score fee discount rule was solely $15,000, and the speed was decreased to 20% in case your AGI exceeded $43,000.

For 2021 the utmost CDCC for a taxpayer with AGI of $125,000 or much less is $4,000 for one qualifying particular person ($8,000 x 50%) and $8,000 for 2 or extra qualifying people ($16,000 x 50%). Earlier than the ARPA, the utmost credit score quantities had been solely $1,050 and $2,100, respectively.

For 2021 the utmost CDCC for a taxpayer with AGI of greater than $183,000 is $1,600 for one qualifying particular person ($8,000 x 20%) and $3,200 for 2 or extra qualifying people ($16,000 x 20%). Earlier than the ARPA, the utmost credit score quantities when the credit score fee was decreased to 20% had been solely $600 and $1,200, respectively.

Thus far, so good.

Instance 1: You’re single. In 2021, you pay $15,000 of eligible bills, for care of your two qualifying youngsters, so you’ll be able to work. You’ll be able to depend the complete $15,000 to calculate your CDCC. Say your 2021 AGI is $132,000. Your credit score fee is decreased from 50% to 46% as a result of having $7,000 of extra AGI. Particularly, the four-percentage-point fee discount is as a result of you may have three x $2,000 of extra AGI plus one fraction of $2,000 of extra AGI. So, your allowable CDCC is $6,900 ($15,000 x 46%). That helps.

Credit score fee is additional decreased or eradicated for high-income taxpayers

For 2021, the 20% credit score fee applies in case your AGI is between $183,001 and $400,000. However as soon as your AGI exceeds $400,000, a second credit score fee discount rule kicks in. The credit score fee is decreased by one share level for every $2,000 (or fraction thereof) of AGI in extra of $400,000. So, the speed is decreased to 0% in case your AGI exceeds $438,000.

Instance 2: Similar as Instance 1, besides this time your 2021 AGI is $420,000. You credit score fee is decreased from 20% to 10% as a result of your $20,000 of extra AGI. Particularly, the ten-percentage-point discount is as a result of you may have 10 x $2,000 of extra AGI. So, your allowable CDCC is $1,500 ($15,000 x 10%). Higher than nothing.

Instance 3: Now let’s say your AGI is $438,500. Your credit score fee is decreased by from 20% to 0% as a result of your $38,500 of extra AGI. Particularly, the 20-percentage-point discount is as a result of you may have 19 x $2,000 of extra AGI plus one fraction of $2,000 of extra AGI. So, the CDCC is totally phased out as a result of your excessive revenue. Sorry.

Liberalized CDCC vs. liberalized dependent care versatile spending account (FSA)

For 2021, the ARPA additionally will increase the utmost quantity which you could contribute to an employer-sponsored dependent care versatile spending account (FSA) from $5,000 to $10,500. The contribution reduces your taxable wage for federal revenue and payroll tax functions (and normally for state revenue tax functions too, if relevant). Then you’ll be able to take tax-free withdrawals to reimburse your self for eligible dependent care bills.

Relying in your particular circumstances, you’ll be able to have dependent care bills which can be eligible for each the CDCC and for tax-free dependent care FSA withdrawals. When you fall into this situation, you can contribute some quantity to a dependent care FSA, accumulate the ensuing revenue and payroll tax financial savings, and take tax-free withdrawals to reimburse your self for eligible bills.

You possibly can then declare the CDCC for “extra” eligible bills beneath the CDCC guidelines, topic to the relevant CDCC restrict on eligible bills. To calculate your allowable CDCC, fill out IRS Type 2441 (Baby and Dependent Care Bills) and embrace it along with your Type 1040. The allowable credit score quantity will present up on web page 2 of Type 1040.

Are you higher off forgetting in regards to the FSA choice and simply claiming the CDCC? It depends upon your revenue and different components. Discuss to your tax professional.

The underside line

The adjustments to the CDCC guidelines for the 2021 tax 12 months should not easy. A associated situation is how one can finest benefit from each the CDCC and the dependent care versatile spending account (FSA) choice in case your employer provides the FSA deal. That provides one other layer of complexity. Lastly, bear in mind that you simply could possibly declare the kid tax credit score for 2021 along with profiting from the CDCC and the FSA deal. That’s some stimulus, people.

Keep tuned: MarketWatch is beginning a cash problem on April 5 to Spring Clear Your Funds in Simply Four Weeks. Observe us on Instagram and subscribe to our publication for updates.

— to www.marketwatch.com

The post The child and dependent care tax credit is more lucrative than ever — but there’s one important caveat appeared first on Correct Success.

source https://correctsuccess.com/credit/the-child-and-dependent-care-tax-credit-is-more-lucrative-than-ever-but-theres-one-important-caveat/

Financial management a vital life skill today, says BNM

by TMR / pic by RAZAK GHAZALI

MANAGING funds properly is a vital life talent these days to make sure one won’t be plagued with cash points sooner or later, Financial institution Negara Malaysia (BNM) mentioned.

“For instance, if we need to retire comfortably, we have to save, not overspend and handle our funds accordingly. This can require planning for the long run and self-discipline in making the mandatory life-style changes.

“A very good information of ample buffer is to have financial savings of between three and 6 months of month-to-month bills. As with most habits, you will need to begin small and be constant in saving. Perseverance is vital,” BNM mentioned in its Annual Report 2020.

A part of managing funds could embody borrowing prudently to fund massive purchases similar to a house, automobile and motorbike or to broaden companies.

In doing so, one mustn’t solely pay attention to how borrowings work (for instance how curiosity is calculated), the phrases and circumstances, but in addition the rights that buyers have.

As information, the full month-to-month debt reimbursement shouldn’t be greater than 60% of a borrower’s web revenue, after making an allowance for statutory deduction for taxation, contribution to the Staff Provident Fund and the Social Safety Organisation.

“By taking management, we are able to keep away from appreciable difficulties and challenges in life. Taking management of our funds can enhance our lives by giving us extra freedom and peace of thoughts,” the central financial institution mentioned.

BNM mentioned an knowledgeable shopper will even be capable to differentiate between real investments and monetary scams.

This comes from understanding that dangers are inherent in monetary actions, and guarantees of excessive returns with out threat are most of the time, a warning signal.

“Among the many key options of monetary scams to look out for are excessive or unrealistic return for a small quantity of funding, assure of simple and risk-free funding, and unsolicited or surprising calls that include affords that appear ‘too good to be true’.

“It is very important preserve all private knowledge, monetary data, password, PIN and TAC particulars secured. Don’t reveal these particulars simply even when some one claims to be from enforcement authorities,” it added.

The post Financial management a vital life skill today, says BNM appeared first on Correct Success.

source https://correctsuccess.com/financial-management/financial-management-a-vital-life-skill-today-says-bnm/

Today’s Mortgage and Refinance Rates: May 2, 2021

When you purchase by our hyperlinks, we might earn cash from affiliate companions. Learn more. Standard charges from Cash.com; government...

-

There was a time once you didn’t fear a lot about your e-mail account, or the web site you obtain years in the past, or your usernames a...

-

Monetary literacy has seen a steep decline in instances, and that’s with out placing the worldwide well being disaster under consideration...

-

Properly-managed credit score can do wonders in your credit score rating. Nevertheless it’s not at all times simple to get permitted for b...