DigniFi CEO Richard Counihan final month mentioned his mechanical restore financing firm had discovered a marketplace for auto physique restore deductible loans as effectively.

“Our clients are taking us into the collision area,” mentioned Counihan, whose firm points loans between $350-$7,500 and companions with service facilities to assist pitch them. “… We now see that beginning to develop.”

Counihan’s feedback in a Nov. 20 interview got here shortly after Collision Recommendation CEO Mike Anderson drew business consideration to a yearslong pattern of upper deductibles.

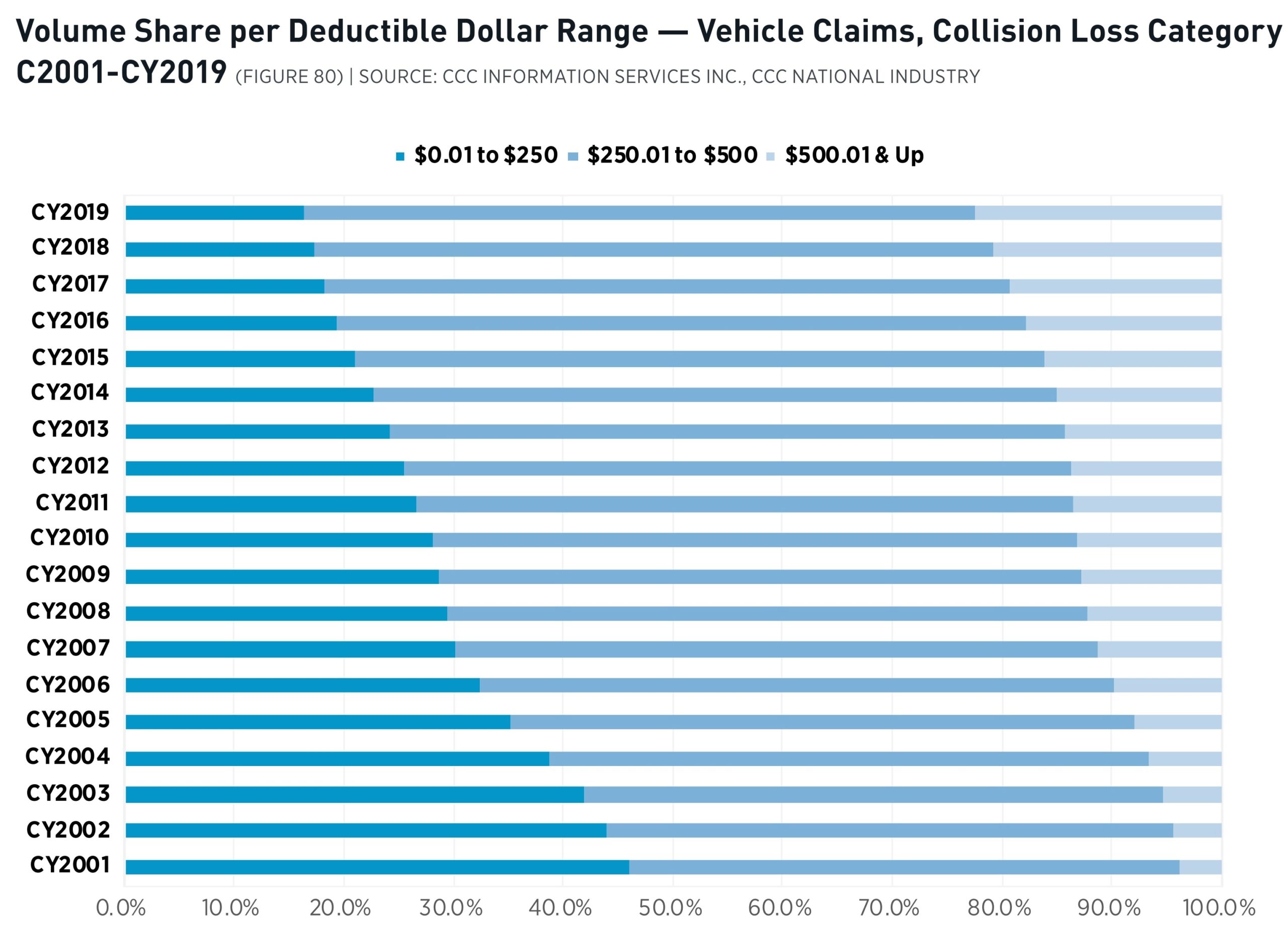

CCC’s 2020 “Crash Course” reported that 22.5 % of collision claims in 2019 noticed deductibles larger than $500 — up from 3.eight % in 2001.

Granted, $500.01 in 2001 works out to more than $727 in 2019 dollars. However the pattern remains to be fairly putting. Taking a look at it from the opposite finish, clients in practically half of all collision claims in 2001 may theoretically get a restore performed for not more than $250 out-of-pocket. By 2019, solely round 20 % of collision claimants had so little an obligation.

“When somebody comes into your store, they very effectively may very well be paying out-of-pocket if they’ve a thousand-dollar deductible,” Anderson mentioned on an Oct. 29 webinar which displayed CCC’s information. “So, don’t underestimate that.” He suggested repairers to arrange their front-end workers for this.

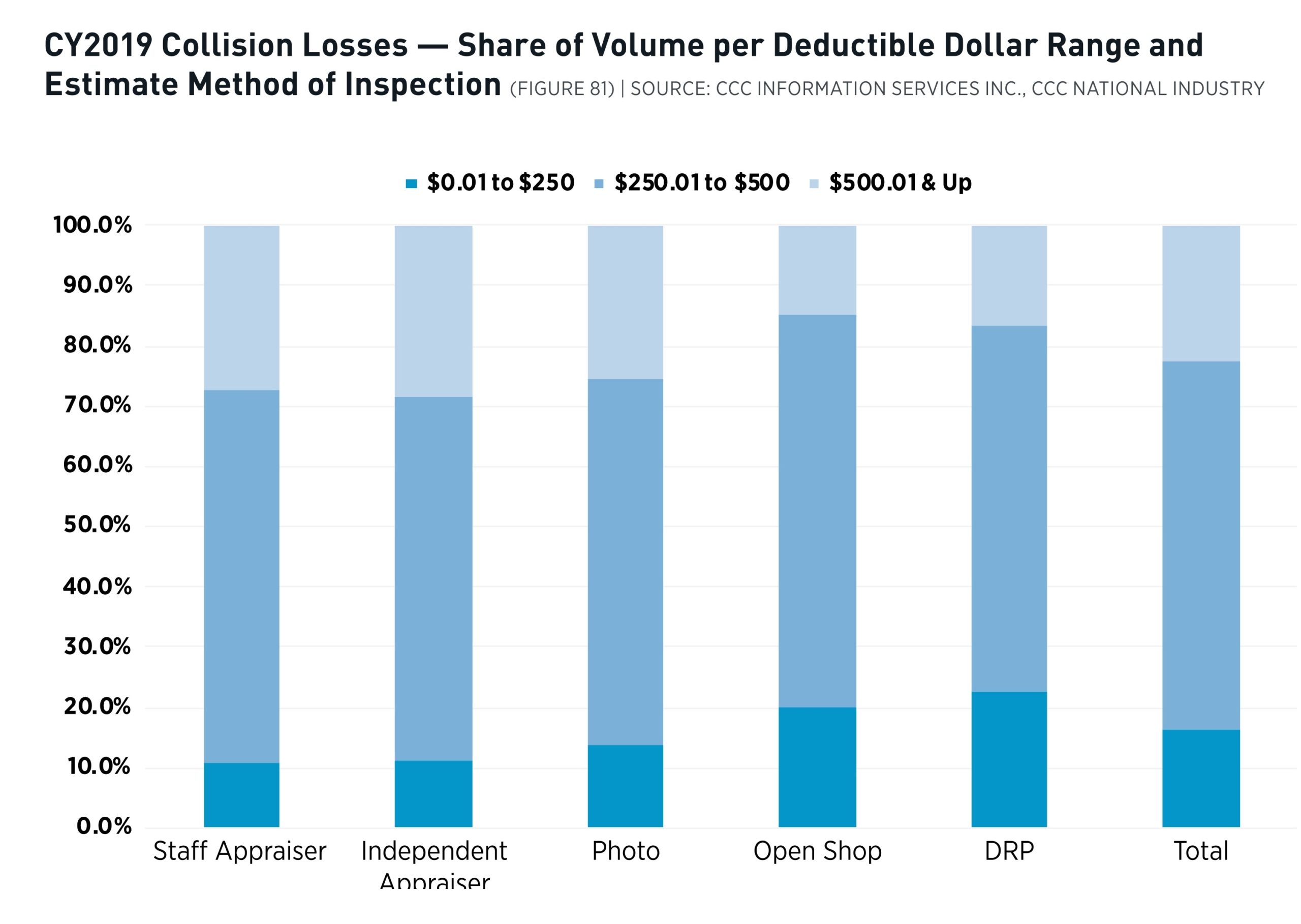

CCC’s “Crash Course” recommended deductibles basically posed an “fascinating query.” It continued:

Are shoppers with larger greenback deductibles extra keen to have their preliminary inspection performed by the insurer versus a store? And, conversely, are these shoppers with decrease deductibles extra keen to take their automobile to a store from the outset (see Determine 81)? Whereas we don’t understand how a lot the deductible elements into shoppers’ selection of technique of inspection, comparability of the amount of value determinations written per greenback vary by inspection sort suggests practically 30 % of photograph value determinations fall under $1,000 (together with any complement adjustments), and practically 60 % fall under $2,000.

CCC’s 2020 “Crash Course” posed this question in mid-March — proper earlier than COVID-19 shook up preliminary inspection preferences and choices. Nonetheless, the data supplier’s query deserves consideration in each the present disruption and forward of the post-coronavirus panorama. Maybe much more so, contemplating reports of virtual claims popularity.

Loans to cowl deductibles

Deductibles “are creeping up” on the entire, Counihan mentioned, describing insurance coverage insurance policies with thresholds of $1,500 and $2,000.

Nevertheless, many People don’t have an additional $500-$600 readily available for bills, based on Counihan, whose firm points unsecured auto restore loans of $350-$7,500 to shoppers following a easy, four-question software course of. “We approve you in below a minute,” Counihan mentioned.

Counihan mentioned his firm has discovered a line of enterprise in chopping loans which cowl each a deductible and value of a rental automobile. He described each as monetary hurdles for a client.

As he described it, shoppers can’t cowl the deductible essential to get their private automobile out of the physique store that fastened it. Sooner or later, it turns into obligatory for the patron to incur the rental automobile expense, he mentioned. (A spokeswoman described

“It’s an surprising expense,” he mentioned of the deductible.

Counihan mentioned clients are sometimes capable of borrow just a few thousand {dollars} through the bank card route. Nevertheless, its widespread for them to additionally carry a stability consuming nearly all of this quantity and actually solely have a fraction obtainable to be used month-to-month. “You’ve acquired no safety blanket,” he mentioned.

He described clients as pursuing deductible-rental mixture loans from his firm quite than deductibles alone.

Requested why clients wouldn’t merely borrow the deductible quantity and reclaim their automobile earlier than rental bills turned obligatory, Counihan mentioned he thought it was as a result of shoppers didn’t understand the loans have been obtainable early sufficient.

We requested if clients have been additionally borrowing to cowl restore bills insurers refused to reimburse, however this wasn’t on Counihan’s radar the best way the deductible-rental bundles have been.

Counihan described his firm as an FDIC-regulated lender. (Its web site calls its loans issued by FDIC member WebBank.) He referred to as it a greater different to some opponents, which he mentioned would possibly act like payday lenders or be structured like a bank card (which isn’t useful to a client whose credit score isn’t adequate for one).

According to DigniFi’s website, the corporate doesn’t cost curiosity for 90 days, although it does require a minimum of minimal funds. After that, curiosity runs between 9.99-36 % APR, backdated to the beginning of the mortgage.

Extra data:

Photos:

Can your buyer really afford their deductible? Maybe not, based on the auto restore lender DigniFi. (CiydemImages/iStock)

CCC has discovered the variety of collision loss claims with a deductible of greater than $500 rose to 22.5 % in 2019. (Supplied by CCC)

CCC’s 2020 “Crash Course” appeared on the preliminary technique of inspection by the lens of a collision deductible. (Supplied by CCC)

Share This:

Associated

— to www.repairerdrivennews.com

The post DigniFi reports interest in auto body deductible loans appeared first on Correct Success.

source https://correctsuccess.com/how-to-repair-credit/dignifi-reports-interest-in-auto-body-deductible-loans/

No comments:

Post a Comment